5 Key Findings on Valuations and Funding of Early Stage Startups in a New Report from Carta

When I meet other angel investors, the first thing we do is ask either other: What are you seeing with startup valuations? And when I meet startup founders, their first (and only) question is: What’s happening with startup investments?

As an active angel investor, I see what’s happening in my corner of the world, but it’s a narrow view, more anecdotal than hard data. I devour Crunchbase and Pitchbooks reports which are incredibly helpful but mostly focus on the VC world of big priced rounds.

So I was thrilled to see a new report released by Carta that focuses on trends in pre-seed/seed investments where angel investors play.

Unlike Crunchbase and Pitchbook which get their data from public announcements which are rare for early-stage investments, tens of thousands of startups at all stages use Carta to manage their cap table. (If you don’t, you should!)

That means every time a startup signs a new SAFE, it goes onto their cap table. Which means it goes into Carta’s database, including terms and valuations. Over 2000 startups using Carta raised capital with a SAFE or convertible note in the first half of this year, exactly the data I want to see.

Here are my 5 key takeaways from the Carta report, but I encourage everyone to read the full report yourselves:

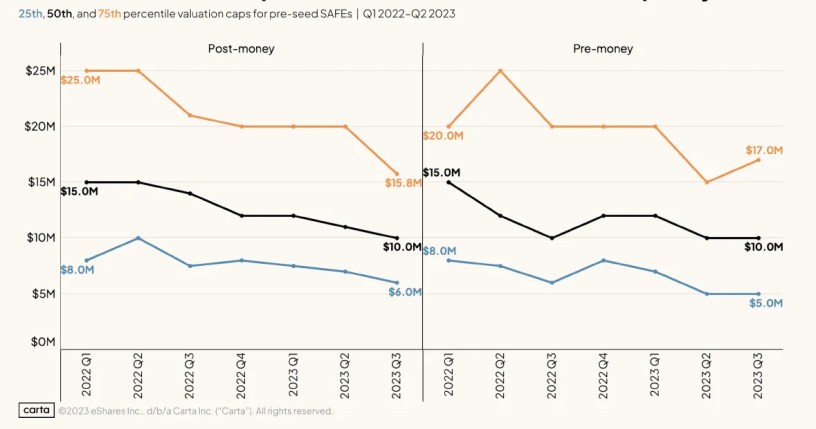

1. Valuations are down by 1/3

In the 1st quarter of 2022, the median valuation cap for a post-money SAFE was $15.0M. In the 2nd quarter of 2023, it was down to $10.0M, a drop of one-third.

Perhaps not surprisingly, the drop was even steeper for startups with the highest valuations. The 25th percentile dropped from $25.0M to $15.8M. On the lower end, the 75th percentile only dropped from $8.0M to $6.0M

However, for raises of under $250K, which presumably are mostly friends and family, the median valuation actually went up over that period from $5.0M to $5.5M. The valuation on raises from $250K — $500K increased from $6.0M to $6.5M.

Since the valuations of these small raises are frequently set by the founders without negotiation from experienced investors, investors in these small, early rounds are probably getting a bad deal.

2. Early-stage funding is down 36% but stabilized

In 2Q23, 1608 startups using Carta raised pre-seed/seed funding for a total of $972M. That’s down 36% from the high of 2,211 companies raising $1.5B in the second quarter of last year.

However, total funding is up from the previous quarter’s $872M, though the number of companies declined slightly from 1,820.

Still, even with the drop in funding, we’re only back to 2021 levels and still up nearly 4x over even 2020. However, I’m not sure how accurate this trend is since Carta itself grew considerably during that period, so the numbers might reflect how many pre-seed startups were on the platform.

3. Median check sizes for angel deals are $25K

For raises of under $250K, the median check size is $15K. For raises of $250K to $1M, they’re $25K.This probably reflects the difference between friends and family investors and angels.

For rounds of $1M — $2.5M that are likely a mixture of angels, angel group member funds, and small VCs, the median check size is $36K.

4. The Post-Money SAFE has become the standard pre-seed/seed investment vehicle

At least among Carta users, the post-money SAFE is now, by far, the most popular investment vehicle.

In the first half of 2023, 83% of startups used a SAFE (pre or post-money) with only 17% using convertible notes.

However, in life sciences and electronics, about half the startups used convertible notes and half used SAFEs.

88% of SAFEs were post-money SAFEs. Only 12% used the older pre-money SAFE format. (Thank God! Let’s get that to 0%.)

Only 12% of SAFEs had no valuation cap. (This should be a non-starter.)

51% of all SAFEs had a valuation cap alone, and another 37% had a valuation cap AND a discount. Most of the time, that discount was 20%.

5. Convertible note terms haven’t changed

Almost all convertible notes have a pre-money valuation cap, a discount, and an interest rate.

The pre-money valuation cap has held steady over the past year and a half at $15M. There was a jump to $18M in the last quarter, but since the data set is small, I’ll assume valuations are essentially unchanged.

The reason convertible note valuation caps have held up while SAFE valuation caps have dropped is likely due to the fact that most of the startups using convertible notes are in life sciences where funding and valuations have remained strong despite the funding downturn across other sectors.

The discount on convertible notes is almost always 20%. The interest rate has held steady at 6.0% since 2020 despite the steep rise in the Fed rate. This implies that nobody really cares much about the interest rate on convertible notes.

Caveats

- This data is based on startups that manage their cap tables on Carta. While Carta is the largest platform for cap table management, the self-selection of using Carta or not may skew the data.

- The analysis is based on startups raising a round using a SAFE or convertible note that has not previously raised a round of preferred equity. However, more early-stage startups are using preferred equity at earlier stages to attract investors, and this may skew the results for the number and size of raises.

- Carta’s customer base is growing (I hope), so comparing the number of raises and amount of money over time may not be accurate.

- I am a small investor in Carta and would like to see more startups use the platform. I don’t think that affects anything I’ve written here but am including it for full disclosure.

- A huge thank you to Peter Walker for creating this great report and granting permission to reprint the graphs here.

To Kill a Unicorn – a Silicon Valley Thriller

SüprDüpr is a late-stage startup preparing for the first trillion dollar IPO. But is the company a Theranos-like scam? Find out in my Silicon Valley novel, To Kill a Unicorn.

Get your copy today!

https://www.amazon.com/Kill-Unicorn-DC-Palter/dp/1950627616