There are many methods to determine startup valuation. This is the only one that works.

“Hey DC — I’m raising a $5M pre-seed with a $50M cap. Interested???”

“Um,” I reply, “how did you come up with the $50M valuation?”

“We did a detailed discounted cash flow analysis and calculated the valuation at $50,874,392.66.”

Hmm. DCF is the perfect answer to the question: tell me you know nothing about startups without telling me how you’re going to fail.

“You have no product and no revenues yet, just a prototype,” I couldn’t help pointing out. “Your valuation is more like $5M.”

“But Acme Explosives just raised at a $50M valuation!”

Acme Explosives is already doing $10M in revenues with W.E. Coyote Industries, so that’s hardly a comparable transaction.

“So how did you come up with your $5M number?” he asked in reply.

The answer isn’t simple, like a spreadsheet model. Startup valuation, especially at the early stages, is more art than science.

There’s a lot of methods to try to value startups. DCF. Berkus Method. Discount off next round. Cost to duplicate. Scorecard. Comparable transactions. Blah blah blah. None of them work.

The reason they don’t work is that valuation is not a calculation. It’s a negotiation.

Like any other asset, a startup is worth exactly the amount that people are willing to pay for it. And the only way to set a valuation is to find out how much investors are willing to pay.

What Is the Actual Value of a Startup?

Investors value early-stage startups the same as lottery tickets. There’s a large probability of getting nothing in return, a smaller chance of getting our money back, a 10% chance of getting a 10x return, and a small but critical chance of hitting a 100x or 1000x jackpot. It’s like playing the Lotto with tickets that cost $10K or $100K instead of $2.

Of course, investors (at least the ones I know) don’t create a probability analysis and assign values to each possible outcome to calculate a valuation.

Instead, it’s a process of comparing the risk vs reward of each startup to other startups we could invest in and picking the best overall combination.

But what determines that risk and reward? Well…everything:

- team experience

- customer traction

- market size

- competition

- ease of market entry

- capital requirements

- exit potential

It should be no surprise, then, that this is exactly the information we ask for in the pitch.

But how does that help you calculate the valuation of your startup? It doesn’t. It just tells you how investors think about valuation.

But How Do I Calculate a Valuation — The Palter Valuation Process!

So how should you determine the valuation of your startup? Just follow the steps below. This is the only process that works. Let’s call it the Palter Valuation Process.

Step 1. Determine Stage

Figure out what stage you’re at. Honestly. You can’t work the problem backwards and say you’re doing a Seed raise because you think you deserve a $20M valuation. Use these definitions as a starting point:

- Friends, Family, and Network: any raise before you have a functioning product and initial customer traction.

- Pre-seed: Product is built and has initial customer traction. Startup needs funds to add critical features and begin marketing.

- Seed: Product is fully complete and the company is gaining significant revenues.

- Series A: Over $4M in annual customer revenue.

Step 2: Find Average Valuations for Stage, Sector & Region

How will investors value your startup? For the most part, they’ll compare investing in your startup to the hundreds of other startups we see each month. The top 1% or 2% with the best risk vs reward profile will get investment.

But compared to what? Data asymmetry is a big problem for founders. Investors are comparing you to all our other applicants that you can’t see. That gives us an idea of what your startup should be worth that you don’t have. Here’s how you’ll get around that.

First, collect whatever data you can on typical valuations. Fortunately, Carta makes available some incredibly useful data (thanks Peter Walker and Carta).

In their report State of the Pre-Seed 2025, Carta shows a median valuation of $15M for a pre-seed raise and $30M for a larger seed raise.

That’s a good start, but not good enough. There are huge differences in valuation between an AI startup in San Francisco and a consumer products startup in Indianapolis. So dive into the data.

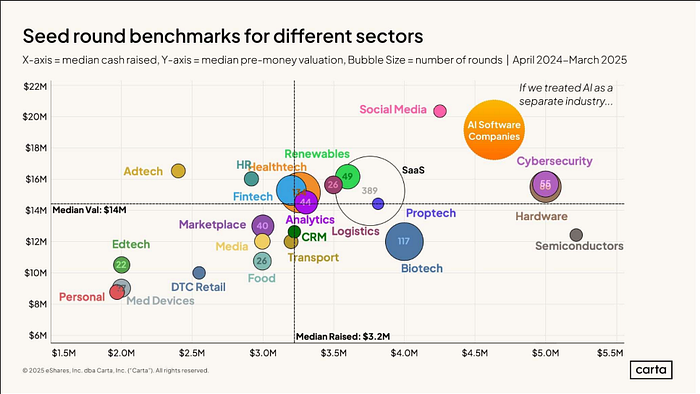

Carta also makes available finer-grained data. One example is the chart below with average valuations at the seed stage by sector. If you’re doing a seed raise in proptech, you’ll be competing with startups raising at a median $14M valuation. Consumer products may be closer to a $10M valuation at the same stage. Similar data shows huge differences in valuation based on geography.

In addition to Carta data, look for other data on other startups in your sector from Pitchbook and Crunchbase, and reports from VCs and investment banks.

Step 3: Make Adjustments

Averages are a good start, but they cover a wide range of startups at different stages in their journey. Instead of looking at Carta’s median values, look at their 25% — 75% data bands.

Should you be at the top of the range or the bottom? Think honestly about all the factors listed above: do you have higher or lower revenues than other startups raising at this stage? How big is the market opportunity really truly? Every startup says they have an all-star team, but are you little league all-stars or all-pro veterans with deep experience in your industry?

Like car drivers, 95% of startup founders think they’re better than average. Unless your startup is truly extraordinary, it’s best to stick near the median of the range or lower. Don’t forget you’re competing for investment with a lot of extraordinary startups in that top 1% to 2% we fund.

Step 4: Sniff Test

Find a few trusted advisors who invest regularly at your stage and ask them for honest feedback. Tell them your proposed valuation. Don’t ask them if they think it’s a fair valuation (of course it’s fair), or if they would invest at that valuation, but if they think you’ll get traction with other investors at that price.

But be careful who you ask for feedback on valuation. It needs to be someone who regularly invests at your stage. You need people who see hundreds of deals at your stage and know exactly where you fit in.

Step 5: Negotiate Valuation with Lead Investor

Now you have a proposed valuation and you’re ready to start the fundraising process. Reach out to investors who are able to lead the round. (See this article about lead investors vs deal followers if you aren’t familiar with the process.)

Make clear that these are your target terms, but the valuation (and other terms) are negotiable.

A lead investor will work with you to find terms that are fair and attractive to both them and you, but they’ll start from your target so it needs to be in the ballpark. Together you’ll negotiate a term sheet that includes valuation along with the other key investment terms.

Step 6: See if the Valuation Holds With Other Investors

You’ve found one investor who thinks that’s an attractive valuation and is willing to invest. Now you need to find other investors to fill out the round. You may have thought the valuation was set, but perhaps not.

It’s not uncommon that a lead investor agrees to some valuation, but other investors aren’t interested at that price. In that case, you might need to have a complicated 3–way or 4-way discussion with the lead and other investors to revise the terms to suit a broader group of investors.

In particular, valuations set with later stage investors, accelerators, corporate venture groups, and strategic investors are viewed skeptically by financial investors. Those investors really don’t care about the valuation. In general, it’s best for the lead to be a financial investor that regularly invests in this stage so they can negotiate deal terms that work for everyone.

Step 7: Hit Milestones and Raise the Valuation

Now that you’ve finished your funding round, it’s time to get back to building. Grow your customer traction, expand the team, and focus on hitting your milestones so that in 18–24 months, you’ll be ready to raise your next round at a much higher valuation.

Off to Series A

Once you hit Series A and beyond, the valuation process changes. Rather than the startup proposing a valuation to begin the negotiations, the VCs of Series A will offer a term sheet to negotiate from.

Valuation Isn’t Everything

Founders tend to focus on valuation as the only metric that matters. But valuation is just one term on the term sheet. The other investment terms are just as important.

In many cases, the liquidation preference — the minimum return for investors—determines how much founders and employees end up getting in an acquisition. (Here’s how a $200M exit can leave the founders with nothing.) A lower valuation with a standard 1x liquidation preference is a much better deal for founders than a higher valuation with a 2x liquidation preference.

For investors, the investment vehicle — post-money SAFE, pre-money SAFE, convertible note, preferred equity, etc. — is important. All else being equal, we’d invest in a startup offering preferred equity over a SAFE, and we’d far prefer a post-money SAFE to a pre-money SAFE. So the valuation we’d find attractive will depend on the investment vehicle.

Be sure to look at the big picture and not just the valuation. And in the end, finding the right investors that are prepared to support you when times get tough is more important than grabbing the highest valuation.