It Takes 10+ Years to See a Return from Angel Investing

I started angel investing in 2009. Since that time, I’ve made 38 investments in 29 companies as an individual and joined 4 angel member funds.

I’d love to brag that these investments have made me a billionaire. On paper, I’m doing reasonably well. In actual cash returned to the bank account, not so much.

When new angels ask me what I wished I’d known when I started, the noobs are expecting the usual platitudes: valuations don’t matter (wrong), invest in the jockey and not the horse (sometimes), or 1 investment will account for all your gains (usually).

But the one thing I really wished I’d known was: for early-stage startup investing, the J-curve is a killer. Because I wasn’t fully prepared.

Strategy Hits Reality on the Battlefield

When I started investing, my strategy was similar to the way I play Monopoly: allocate a block of money to invest in startups over the first 3 years. Then, starting Year 4, reinvest the returns from the earlier investments to make new investments.

Why 3 years? Because every startup says they’ll have an exit (acquisition or IPO) in 3–5 years. For each 2x exit, I could invest in 2 more startups. For each 10x exit, I could invest in 9 startups and and enjoy a luxury cruise of the Mediterranean.

Oh, I was so naïve.

Of those 29 individual investments over 12 years, so far only 3 have had exits, 4 were write-offs, and the other 22 remain sitting in my portfolio waiting for something to happen. That’s the J-Curve.

3–5 years? The only companies that have an exit in under 5 years are the failures.

For VC’s investing in Series A and later, 5 years isn’t unreasonable. For angels investing in earlier rounds, add 2–3 years to that.

There are exceptions, of course; a few big winners get plenty of press and make it sound so easy. For the other tens of thousands of startups that get funded every year, it’s a longer slog.

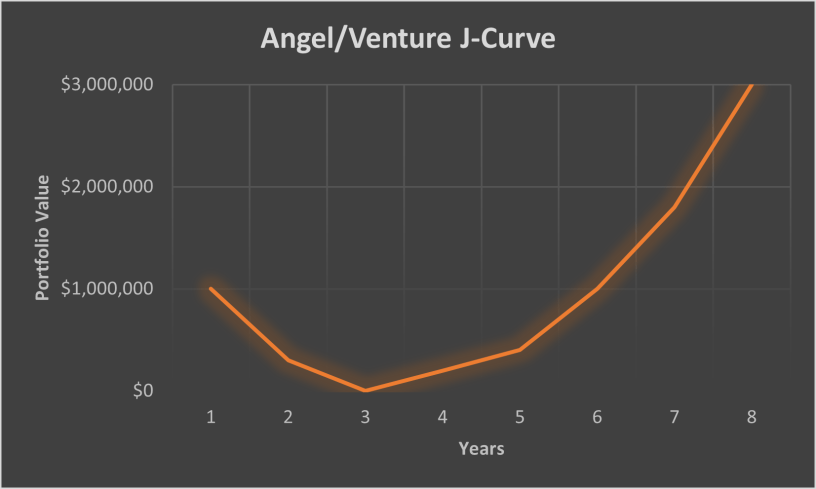

What is the J-Curve?

Let’s say I allocate $1,000,000 to invest in a portfolio of 10 companies over 2 years. At the end of the 2nd year, the piggybank is empty. (See chart at top of article.)

In the first 4 years, there are a number of failures, along with an exit or two that get some or all of my money back. The 1 or 2 good investments are doing well, raising bigger rounds. Rather than providing a return, those need me to invest more.

Eventually, my successful investments cash out with big returns. After 8 years, I’ve made 3x my investment, but for 4 years I’ve gotten nothing. It’s not until year 7 that I’ve even gotten my investment back.

In simple language, my losers fail fast, my winners take a long time to mature. That’s the J-curve, in theory.

Theory vs. Reality

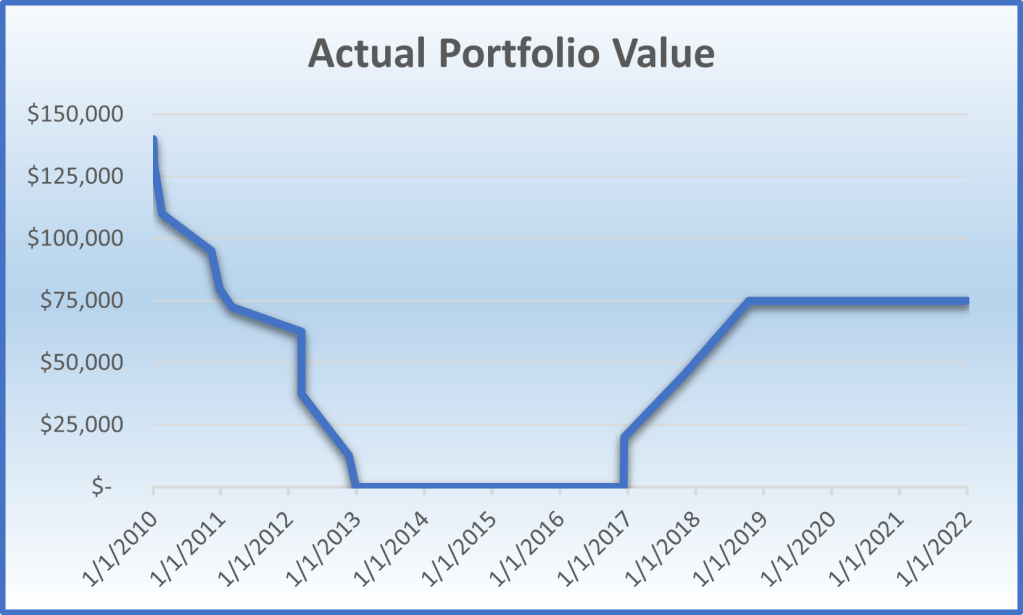

So what’s the reality? I examined my own investments for the 3 years from 2010 to 2012. During that time, I allocated $150K for angel investments.

Over those 3 years, I made 9 investments in 8 companies, using up the full $150K with small investments. By the end of 2012, the bank account was empty.

Over the next few years, a few of the companies failed outright. My first (somewhat) successful exit wasn’t until the end of 2016, 6.5 years later. My next was in late 2017, 5 years after making the investment. My third was at the end of 2018, 8 years later.

Out of the 9 investments, there were 3 small successes, 4 write-offs, and 2 companies remaining in the portfolio.

However, those 2 companies are doing quite well. If both have a 10x exit as their current valuation implies, I’ll get a total 2x return. If one of them has a 100x exit, I’ll be able to brag about how brilliant an investor I am with an 8x total return.

So, 12 years after I started angel investing, I still don’t know whether my initial portfolio has a 50% loss or an 8x return. It all depends on the success of the 2 remaining companies in the portfolio.

Am I Just a Bad Investor?

Every day, I hear people saying they’ve made millions at angel investing. I clearly haven’t, at least not yet.

Is that because I’m a bad investor? Did I put my money into losers and miss the big winners? Or was I inexperienced, making bad bets at the time?

Maybe. With my experience now, I would have avoided some of those 9 investments. But even with experience, picking winners is never easy. Even VCs will admit that 90% of their investments won’t break even. And they start at a later stage.

At the same time as making those 9 individual investments, I also put additional money into an angel fund. That fund invested a total of $3.3M in 24 companies. The results of the fund are surprisingly similar to mine: after 11 years, it has yet to return the full investment, but has 2 companies remaining in the portfolio that are eventually expected to lift returns to 2x-3x the original investment.

Okay, maybe I’m not so bad. Or I pick bad funds as well as bad startups.

Is Angel Investing Worth It?

Has angel investing been worthwhile? As Zhou Enlai supposedly said about the French Revolution, it’s too early to tell. It’s only been 12 years.

What is certain is that early-stage angel investment requires far more patience than I originally expected.

If I was only looking for financial returns, I’d be better off buying Apple stock or if I wanted to gamble, there’s crypto. But that’s not why I’m an angel investor.

I invest in startups because I want to help them succeed. I’m satisfied if I can break even. It would be great to brag about a 100x return, but more importantly, every 10x return is 9 more startups I can help get off the ground while I’m on that cruise of the Mediterranean.