And Why I Demand Liquidation Preferences, Too

When negotiating investment terms with startups, there is nothing as contentious as the liquidation preference. And for good reason.

In the vast majority of startup exits, it’s the liquidation preference that determines how much investors get, how much founders and employees get, and in many cases, whether they’ll get anything at all.

The liquidation preference can set investors in different rounds at each other’s throats, divide the board, and cause founders to sacrifice the employees who helped them build the business. All that from a couple of sentences in a term sheet.

Personally, I hate liquidation preferences. I’ve been burned by later investors using big liquidation preferences to grab all the gains for themselves. But without liquidation preferences, I get burned by early exits, so I depend on them to protect me, too.

Liquidation preferences seem like a minor detail on the term sheet, but other than the valuation, they’re probably the most important term. Both founders and investors need to understand them and know what they’re agreeing to.

What is a Liquidation Preference?

At its simplest, the liquidation preference is a minimum payout the investors receive when the company is acquired.

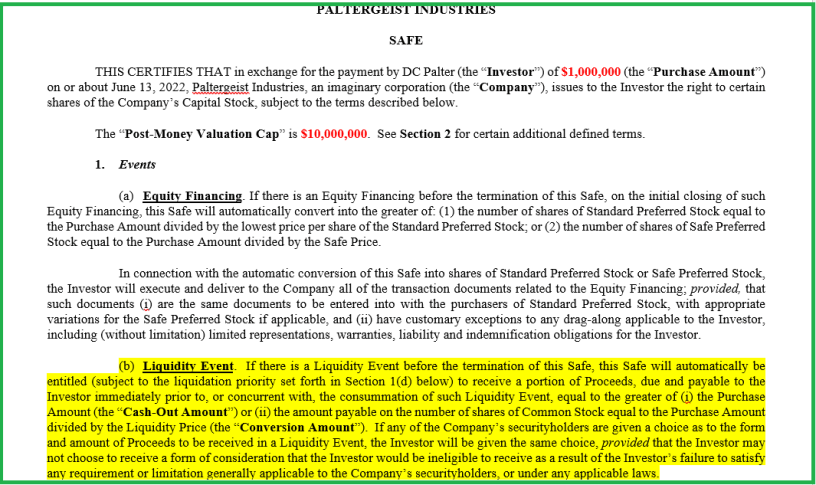

In most cases, the liquidation preference is “1x”, meaning the investor is guaranteed at least her money back. The standard SAFE note includes a 1x liquidation preference. However, 1.5x and 2x liquidation preferences aren’t uncommon, and I’ve even been in a deal with a 4x liquidation preference.

If I invest $1 million in a startup with a $10M valuation, and it’s subsequently acquired for only $5M, if I have a 1x liquidation preference, I get my $1M back instead of the $500k my stock would otherwise be worth. This is one of the special conditions that makes my stock “preferred”.

Had the startup been acquired for $20M, I’d obviously take the $2M my stock was worth rather than the $1M liquidation preference.

Participating vs Non-Participating Liquidation Preference

In the example above, I get the larger of the minimum guarantee (1x my original investment) OR the value of the stock. That’s called a non-participating liquidation preference.

With a participating liquidation preference, investors get their minimums AND a pro-rata share of anything left over along with other shareholders.

If my $1M investment at a $10M valuation (10% ownership stake) was the only investment in a company acquired for $5M, with a non-participating liquidation preference, I’d get my $1M back. The remaining $4M would go to common shareholders.

With a participating liquidation preference, I’d get my $1M back, plus my 10% of the shares would entitle me to an additional $400K of the remaining $4M. I’d get a total of $1.4M of the $5M acquisition value.

In this scenario, one word — participating or non-participating — significantly changes my return as well as that of other shareholders. So make sure to understand the details.

Is a Liquidation Preference Fair?

If I invest $1M in your startup at a $10M valuation and it’s sold off in a fire sale for $2M, is it fair that I get my original $1M back? Well…that depends on which side of the table you’re sitting.

The valuation at which I invested was based on risk vs reward. The liquidation preference reduced my risk and therefore raised the valuation. In other words, in return for this downside guarantee, I’m getting a smaller percentage of the business.

The liquidation preference is a negotiable term. Like any other deal term, it has no inherent fairness or unfairness outside the context of all the other terms including valuation.

However, sometimes deal terms can seem egregious, especially when the company is desperate for cash and investors cram a take-it-or-leave-it deal onto the company. Large liquidation preferences of 2x or 4x are often part of ugly, painful terms, meaning that investor get two times or even four times their money back before anyone else gets anything from an acquisition.

Why I Need a Liquidation Preference

While I’m not a fan of liquidation preferences, as an early-stage investor, I need them to protect me from getting burned by an early exit.

Consider the following scenario that’s happened to me more than once: I invest $1M in a startup at $10M valuation. Six months later, someone offers to buy the business for $5M. That seems easy to say no thanks to.

But to the founder? $5M in cash is real money. Life changing money. No more fundraising. No more eating ramen, at least the instant kind. No need to bust his butt for 5–10 years more years for the chance of a bigger payout. It’s tempting.

And the founder owns a majority of the stock and controls the board. There’s nothing to stop him from taking the deal. Many do.

Getting my money back from a 1x liquidation preference when the founder pockets millions makes me angry. But without a liquidation preference, I’d only get back half in this scenario. That would make me livid.

If I think there’s a real risk of an early escape, if I don’t avoid investing entirely, I require a larger liquidation preference.

Drowning Under the Waterfall

While I demand a liquidation preference to protect me, as an early investor, in most cases it’s me getting burned by the liquidation preferences of later investors.

Consider this situation: I get a 1x preference on my $1M seed investment. The VCs in the next round get a 2x preference on their $25M Series A. Then the VCs in Series B get a 4x preference on their $100M.

A year later, the company is sold for $400M. I should be celebrating. The company I invested in with a $10M valuation is being sold for 40x what I paid. Woohoo! My $1M investment is worth $40M, right?

Nope. That last investor gets all of it. With a 4x liquidation preference, if the company is sold for anything less than $400M, they get all of it. Every penny.

As the last money in, their liquidation preference has priority over previous investors. This creates what’s known as a waterfall as the money flows down from later rounds to earlier rounds to common shareholders.

If the acquisition was $450M, the Series B investors would get $400M, Series A would get $50M, and I’d still get nothing. At $500M, there would be $50M left over for me and the common shareholders. How that gets divided depends on whether each liquidation preference is participating or non-participating.

Why Would Other Investors Agree?

So why would I, as an investor in an earlier round agree to a 4x liquidation preference for a later investor?

Most likely, I don’t have a choice. The company needs the cash to survive, and this is the only deal on offer. When you need $100M in a hurry, you don’t have a lot of negotiating leverage.

Terms like these were common after the last financial meltdown when companies were burning cash and investment suddenly became hard to find. It’s likely history will repeat itself soon.

Why Would Founders Agree?

If the liquidation preference of later investors are bad for me, they’re even worse for founders and employees at the bottom of the waterfall.

The founders agree because it’s the only way to keep the lights on and keep paying themselves and their team. But there’s no way they’ll agree to an acquisition where they get nothing, and no acquirer wants a startup without the executive team.

So any acquisition includes a big retention package. If the founders and executives don’t make anything from their stock, they’re offered millions to stick around for 2–3 years. A $400M deal might get split as $375M acquisition (purchase of shares) with $25M in retention bonuses.

The founders do okay. Not the billions they were shooting for, but they don’t go penniless either.

In these types of deals, later investors double their money, or quintuple it. Not a bad return for a year or two. But early investors get nothing. And employees are told it’s a big win that they get to keep their jobs.

It’s easy to see why the argument over liquidation preferences turns into a food fight between later investors, earlier investors, founders, and employees.

Liquidation preferences are not only here to stay, but will become more common as money grows tighter and big investors make bigger demands. If a downturn is a tough time to be a startup CEO, it’s an even tougher time to be an early-stage investor.

A Novel Idea!

Like my articles about startups? You’ll love my new novel about a hot Silicon Valley startup where murder is part of the business plan. Being published Feb. 1, 2023 by Pandamoon Publishing.

Reserve your copy today!

Kindle: https://www.amazon.com/Kill-Unicorn-DC-Palter-ebook/dp/B0BK258MTT

Paperback: https://pandamoonpub.com/products/to-kill-a-unicorn-1